The National Institute of Economic and Social Research has just published an article by Prof Roger Farmer entitled “Three Facts About Debts and Deficits”. Farmer goes off the rails with his third fact.

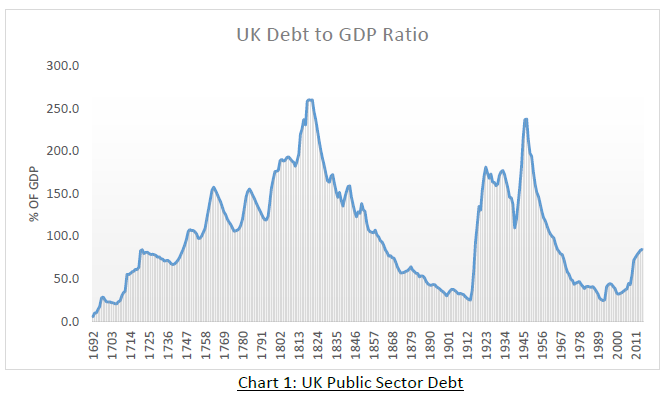

The first “fact” or claim comes in a section entitled “UK Public Sector Debt is Not Large”. I agree with that. Farmer shows this chart to back his claim.

As the chart illustrates, UK public debt is currently small compared to what it was in the early 1800s and the first half of the 1900s.

Farmer’s second “fact” is set out in a section entitled “Governments Do Not Repay Debt: They Grow Out of It.” That’s also OK by me, except that even if there was no growth, governments STILL wouldn’t basically repay debt (although there might the odd year in which there is a net repayment of debt).

The reason has to do with inflation. That is, assuming the debt/GDP ratio remains constant (which it more or less does in the VERY LONG term) that debt will be eroded by inflation. Thus on the above “long term” assumption, the debt will need to be constantly topped up: that is, government will need to constantly incur more debt (in nominal terms but not real terms).

The third fact.

However, it’s in relation to the third fact that Farmer goes much further off the rails. The relevant section is entitled “Government Debt Should Not Be Zero. Ever!”

The reason Farmer gives is that government needs to borrow in order to invest.

That is actually a fallacy which the average taxi driver can see thru. That is if the average taxi driver wants a new taxi and has more than enough cash to buy it, he won’t borrow and quite right: he’ll pay cash for the taxi. In short, borrowing makes sense if you’re short of cash, but not otherwise. Indeed, a significant proportion of industrial investment is paid for via retained earnings, i.e. cash, rather than via borrowing.

But governments have a near inexhaustible source of cash, namely the long suffering taxpayer. Plus to some extent they can print money to fund their expenditure. Ergo governments are not short of cash, ergo the arguments for government borrowing are starting to look decidedly weak. Indeed, Milton Friedman and Warren Mosler argued that there should be no government borrowing at all: i.e. that all government spending, including investment spending should be funded by “tax and print”.

Plus the Swiss academic Kersten Kellerman went into this question in more detail than Friedman and Mosler in a paper in the European Journal of Politcal Economy and came to the same conclusion, namely that government borrowing is not the best option.

Sharing the burden across generations.

Farmer also falls for the popular myth that government borrowing enables the cost of an investment to be shared across the generations who benefit from the investment. As he puts it, “The benefits of public capital expenditures are enjoyed not only by the current generation of people, who must sacrifice consumption to pay for them, but also by future generations who will travel on the rail networks, drive on the roads, fly to and from the airports and drive over the bridges that were built by previous generations.”

The first flaw in that argument is that the total amount of investment done by governments nowadays is roughly constant from year to year if one includes ALL TYPES of investment: e.g. investment in military hardware. Plus education is one huge investment. To that extent it is a waste of time trying to accurately estimate how much burden should be born by which generation: i.e. we might just as well pay for all investment out of “tax and print” and have done with it.

Second, it’s a plain physical impossibility to use steel and concrete produced by the blood sweat and tears of people in 2030 to build a bridge in 2016. That involves time travel.

The only way round that physical impossibility as explained by Nick Rowe is to have the youngsters in each decade support or subsidise the oldies in that decade. Here’s an illustration.

Public investments are made in the 2020s thanks to work by those of working age in the 2020s. Government borrows from those individuals. In the 2030s, new entrants the labour force have to buy relevant bonds off those who retire in the 2030s. And in the 2040s, new entrants to the labour force have to buy bonds off those who retire in the 2040s.

That way, new entrants to the labour force in the 2040s effectively pay for the investments made in the 2020s. Time travel is possible after all! But there is a catch as follows.

That process via which youngsters in the 2040s support those who retire in the 2040s occurs anyway via sundry pension systems! And it doesn’t make any difference whether the pension schemes invest in bonds or whether the pension schemes are like the UK’s state pension scheme which is what’s known as “pay as you go”: i.e. taxpayers in each year support pensioners in that year under pay as you go schemes without any bonds being bought.

All in all, trying to apportion the cost of investments made in 2016 to youngsters in 2030 or 2050 is a dog’s dinner: it’s a waste of time.

No comments:

Post a Comment

Post a comment.